One indication that the quantitative investing market is maturing is the shift in focus from individual products towards the effective construction and management of entire portfolios of quant strategies.

Further, the different players in the industry (index providers, brokers, research houses, calculation agents, and so on) are beginning to take on other roles and responsibilities. Many are moving towards providing a full service, which includes offering their own investment products.

The number of quant index providers and strategies has exploded in recent years, driven by strong appetite from mainly institutional investors. There are now thousands of smart beta and risk premia indices traded as either ETFs or in the unlisted market, while the pools of capital chasing these innovative products continue to deepen.

Product innovation remains a driving force in the industry – including the creation of indices which offer a tilt towards newly-identified factors (such as the knowledge effect).

But more attention is also being given to the effective building and management of quant portfolios. Asset managers now have the opportunity to showcase their quant portfolio management skills, which includes offering tailored products and portfolios to clients.

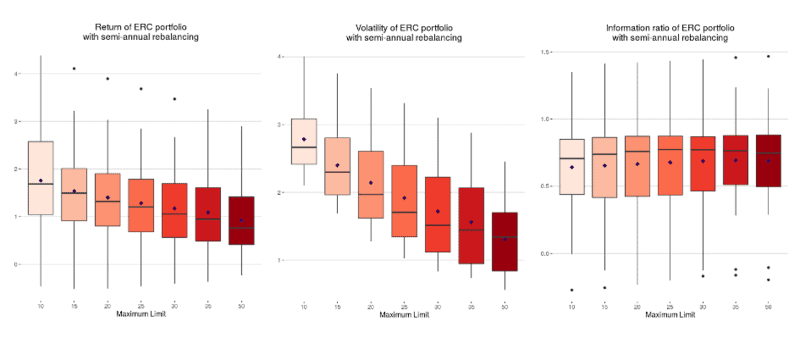

One of the attractions of quant strategies is that the underlying factors they target are often uncorrelated to one another. By building portfolios that contain uncorrelated indices, investors can reduce total risk and smooth portfolio returns.

For example, indices with a momentum tilt tend to be relatively uncorrelated from value strategies – meaning a combination of the two can reduce volatility.