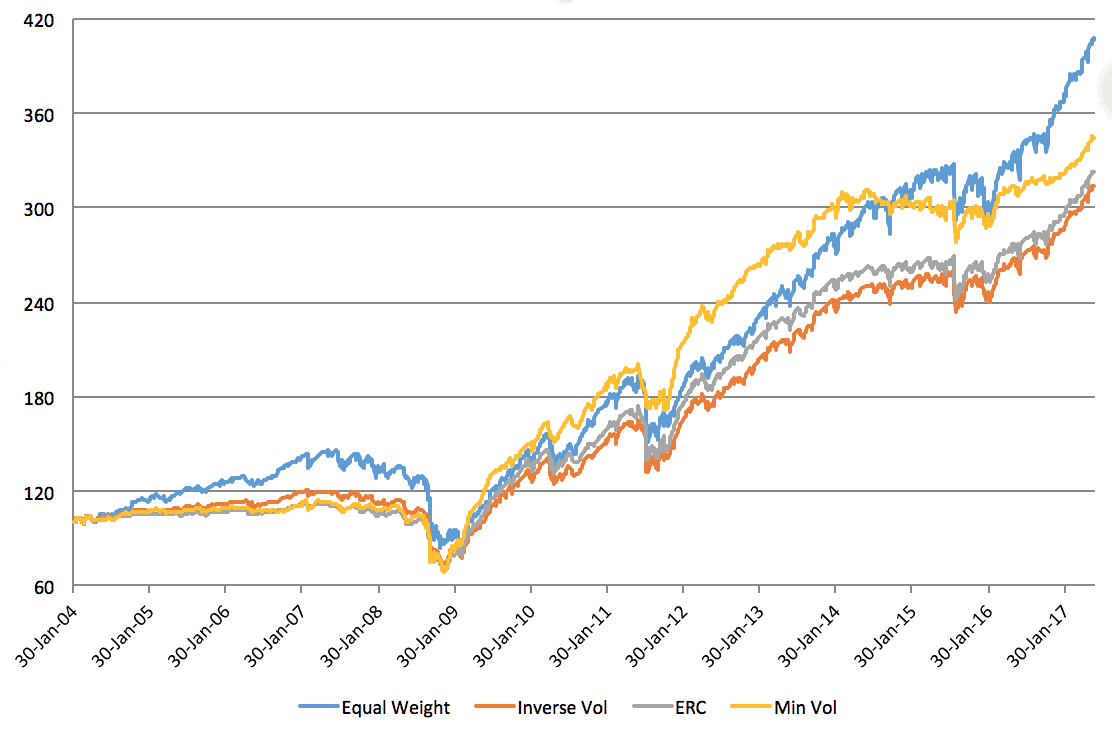

Managing a portfolio of Risk Premia indices requires accurate tools and analytics to help investors define the exact weighting scheme suited to their needs. For a given set of strategies, with similar fees and rebalancing frequency, the outcome from different weighting methods can be very substantial.

Some of the basic ways to rebalance a portfolio include:

Equal weights or fixed weights:

Simple, it reduces the transaction costs by keeping the weights around the same level

Inverse volatility:

It aims at smoothing the impact of each strategy within the portfolio, by overweighting the less volatile strategies and underweighting the most volatile ones

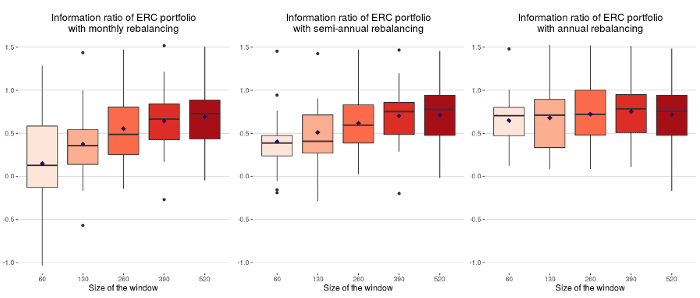

Equal risk contribution:

Taking both volatility and correlation into account, it aims at reducing the overall risk of the portfolio, while keeping its upside potential. Slightly technical, it is more difficult to explain but can prove very efficient during market turmoil. As for any other sophisticated method, one needs to make sure that the volatility and correlation parameters input in the model are relevant and correspond to the portfolio manager objectives.

As no method is perfect, trying and testing several weighting schemes is important before taking any investment decision. Quantilia allows investors to test out several methods in no time, for different rebalancing frequencies, transaction costs and management fees.