Quantitative research can be applied to just about any industry, from physics and insurance to sports and even investing. Essentially a spinoff of applied mathematics, quantitative investing uses raw data to calculate ‘fair’ stock values, earnings forecasts and other metrics that help investors make capital allocation decisions.

Further afield, quantitative screening can be applied to the strict requirements of Shariah-compliant funds in order to select appropriate stocks only.

At the stock level, quantitative analysis uses historical data to calculate key indicators of risk and return, as well as identifying buying opportunities based on trading prices, among a vast number of other applications. Qualitative analysis, on the other hand, looks more closely at the underlying company itself rather than on numbers.

Quantitative (or ‘quant’) strategies usually seek alpha returns, or returns which beat the rate offered by the market. They can do so by identifying underlying factors, or stock characteristics, which are common drivers of high risk-adjusted returns.

The demand for quants (as quantitative analysts are often called) is on the rise, partly fuelled by increasingly complex financial markets and products. The phenomenon also reflects investors’ search for sources of alpha returns and lower fees.

Quants are often sourced from other industries, such as the sciences, and usually need additional skills including computer proficiency. By constructing computer-based models and applying relevant data, quants can create investment strategies and other trading tools.

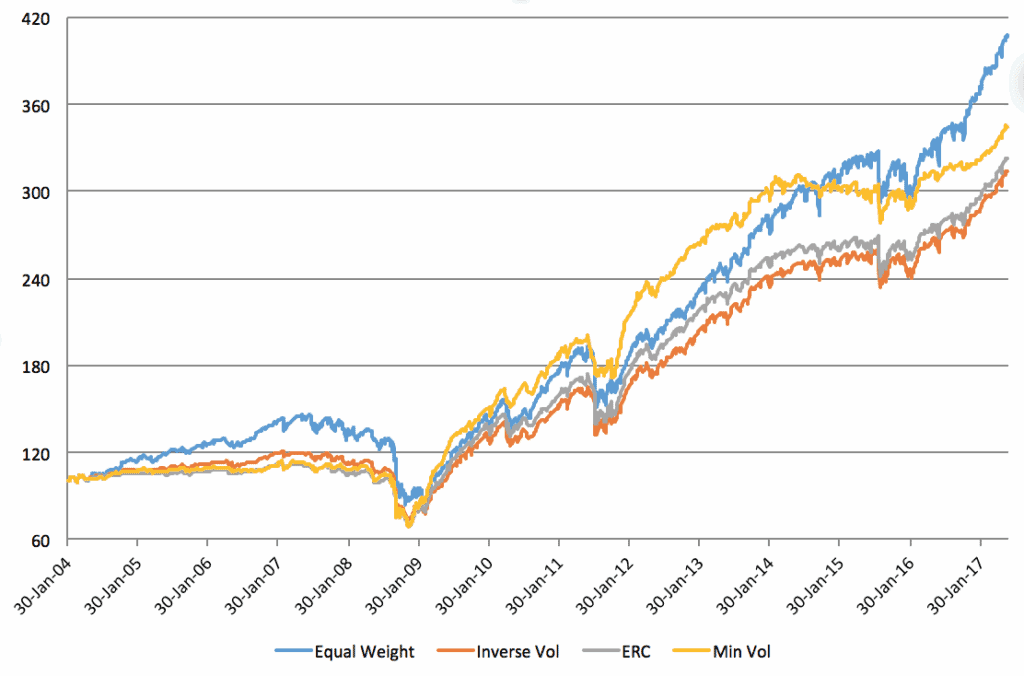

Investment strategies that use a high degree of quant input include hedge funds, smart beta and risk premia.

Smart beta strategies, for example, can target various factors including size, momentum and value. A value strategy selects stocks which are trading in the market at below their fair value, based on data analyses. These stocks will also need to meet other requirements in accordance with the strategy’s rules.

Qualitative versus quantitative research

Mathematically-driven quantitative research differs significantly from qualitative analysis, which relies more on human judgement and intuition. While quant strategies often focus on the performance of a company’s shares, qualitative strategies look more closely at the company itself.

One problem with the qualitative approach is that it is difficult to gauge whether or not investors in the market have already priced their observations into a company’s share price.

Investors in US, UK and European markets, as well as in parts of Asia, are trending towards quantitative investment techniques, though many still see the value in qualitative approaches.

Qualitative research is more subjective but measures what numbers cannot: including competitive advantages, management strength and direction, and a stock’s long-term prospects based on the future of the market in which it operates and its own immeasurable fundamentals.

For example, a qualitative research approach might include one-on-one meetings with a company’s management team in order to gain an intimate understanding of a company. A quant, however, evaluates a potential investment almost purely on numbers and on identifying disconnects between fair values and trading prices, for example.

Both approaches can potentially be time consuming and each has its own merits.

Perhaps the most famous proponent of qualitative investing is Warren Buffett, who has criticised the use of complex mathematical models along with the finance-theory assumption that markets are efficient. Buffett is an ultra long-term value investor who holds shares for decades.

One shortcoming of quant models is that many are based on historical information. While this does help to identify trends that may persist into the future, this is, of course, not always the case.

However, quantitative investing removes the emotional biases associated with subjective judgement, and helps to make sense of large heaps of data.

Quants can turn raw data information into important risk and return ratios, which can then be compared to other stocks to identify future winners and losers based on past and projected performance.

Ultimately – depending on the investor – a combination of the two approaches can be the most logical tactic; using quantitative models alongside sound investor judgment wherever appropriate.

Even quant-based strategies like smart beta and risk premia use a degree of manager discretion, particularly when formulating a strategy and its rules. A number of smart beta and risk premia strategies have delivered superior performance metrics over recent years, and these strategies are continually evolving.

These are alpha strategies, which means they target excess returns. This is often based on targeting underlying factors, or risks (which can be added onto a beta investment through portable alpha strategies).

As markets develop and become even more complex, the demand for quants is likely to continue its upward trajectory.