Shariah investing follows Islamic finance rules, which restricts these strategies from investing in certain products, industries and funds (including

long-short risk premia strategies).This niche market is quickly gaining traction after a relatively slow start in the 1960s, providing opportunities for smart beta providers to target Shariah capital.Shariah-compliant funds fall under the umbrella of faith-based investing, which also includes Catholic and Protestant investment funds.Shariah investing

According to professional services firm PwC, Muslims make up nearly a quarter of the world’s population, yet less than 1% of the world’s financial assets are Shariah compliant. This naturally points towards a massive untapped market since most financial products are not accessible to Muslim investors.

Shariah-compliant funds first appeared in the late 1960s in Malaysia, and spread to the Middle Eastern market within a few years. PwC says high net-worth individuals were the early adopters and still account for a large proportion of Shariah-compliant assets.

Shariah-compliant funds must invest in Shariah-compliant companies and have to appoint a Shariah board. They are also required to undertake yearly Shariah audits and must donate prohibited income streams to charity.

These funds are restricted from investing in companies which sell alcohol, pork products, tobacco, pornography and weapons, as well as those which are involved in non-Islamic banking and those which invest in gaming and gambling. Interest-bearing instruments are also not allowed under Shariah law.

Smart beta investing

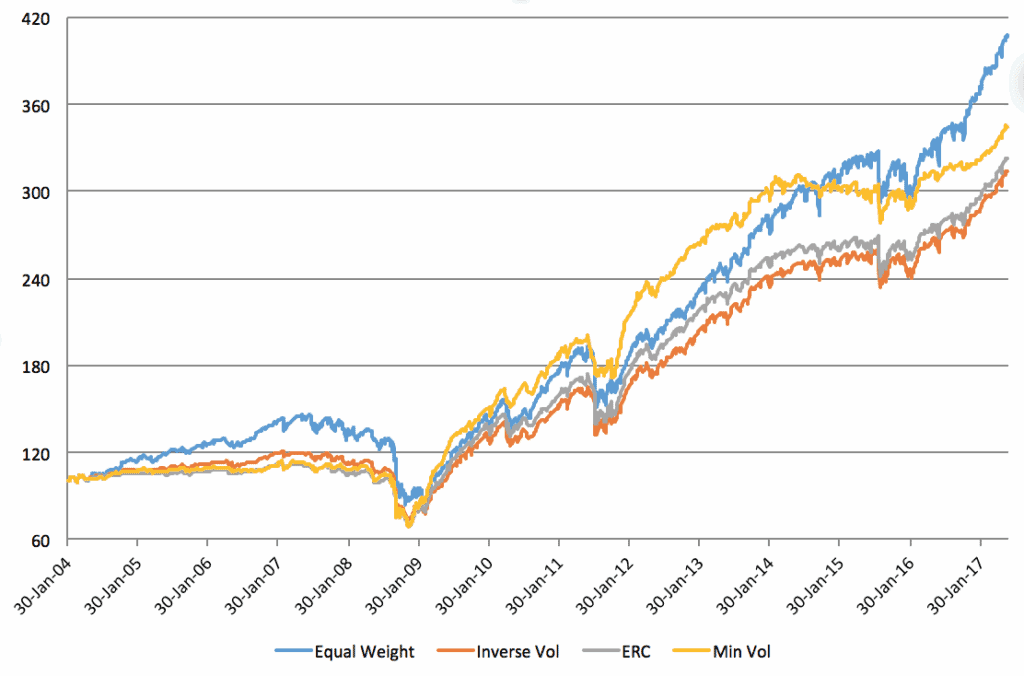

Smart beta strategies use alternative index construction methods in order to control risk, add diversification, or boost returns (generate alpha). Performance is measured against standard benchmark indices, such as the S&P 500 Index – which offers beta (market) exposure. Returns which beat the benchmark are considered alpha returns.

The smart beta investment universe has gained serious traction over the past few years and this growth is set to continue over the coming decade at least, driven by surging demand from investors for low cost and transparent products.

Based on quantitative data analyses, smart beta funds target underlying stock factors which are behind better risk-adjusted returns, including value stocks, small-sized stocks and low-volatility stocks. Some asset managers expect smart beta strategies will naturally evolve into ‘smart alpha’ investing.

Smart beta meets Shariah-complaint funds

A number of major index providers now offer Shariah-compliant indices.

S&P Dow Jones Indices offers both global and regional Shariah-compliant indices, which have high correlations to the indices on which they are based. For example, the S&P 500 Shariah Index includes all Shariah-compliant constituents of the standard S&P 500 index.

In October 2015, S&P Dow Jones Indices launched two new smart beta funds aimed at the Middle East and North African markets: a low-volatility high-dividend portfolio and a composite Shariah dividend portfolio. Constituents in the first fund are selected by ranking the 75 highest dividend yielding stocks in ascending order by volatility. The 50 stocks with the lowest volatility are included in the portfolio.

Low-volatility indices aim to control risk, though many believe they can also generate superior returns (alpha).

Similarly, the FTSE Shariah Global Equity Index Series is based on large- and mid-sized stocks within the FTSE Global Equity index Series. Stocks are screened by external consultants. The Shariah index excludes conventional finance stocks (or those which are non-Islamic) and alcohol stocks, among others.

Other smaller players, like Malaysian fund manager AmInvest, are wading into the Shariah-compliant smart beta market.

Smart beta strategies and other types of indices are in many ways ideal investment structures for Shariah-compliant funds, since smart beta is inherently transparent and rules-based. However, these funds can be relatively difficult to construct as they must exclude large amounts of stocks which do not qualify under Islamic laws.

But as the market supporting Shariah-compliant funds develops, the number of products and sophistication thereof is likely to flourish.

Some analysts and promoters of Shariah-compliant indices argue that these funds generated better performance metrics than their non-Islamic benchmarks in the wake of the global financial crisis, because they were less volatile (in other words, their beta values were lower). Beta measures the volatility risk of a fund relative to the market’s. Alpha, meanwhile, measures excess return over what the market offers.

Limitations of Shariah investing

Launching a fund range which is Shariah-compliant can be a difficult task, given the limitations on the types of structures available to implement such strategies, as well as restrictions on holdings.

For example, usual private equity funds are not suitable vehicles for Shariah funds since private equity fund managers receive performance fees (which is not allowed under Shariah law). Further, other returns-boosting strategies such as portable alpha are restricted because they use long-short trades.

While smart beta strategies target factors using long-only trades, factor strategies using long-short trades are questionable under Shariah law. This is because short-selling is synonymous with selling an investment which is not owned by the seller.

This means long-short risk premia strategies (and hedge funds) are often excluded from Shariah-compliant strategies. A risk premia portfolio, for example, might buy an alternatively-constructed smart beta index (which is Shariah compliant) and short-sell the benchmark index against which it is measured.

Risk premia strategies are becoming popular alternatives to hedge funds, which lack transparency and are only available to high net-worth investors.

Similarly, smart beta strategies are competing for capital with mutual funds. Many market commentators and fund managers argue that since smart beta strategies often target alpha returns, the name of this approach can be misleading.

Modern portfolio theory previously failed to explain why the factors behind smart beta and risk premia strategies yielded superior returns. But some factors including the size and value factors have been added to stock pricing model