Some portfolio managers see alpha investment strategies – which are usually synonymous with seeking market-beating returns – as important volatility risk control mechanisms. One example of an alpha strategy which strives for both volatility-tempering diversification and additional sources of returns is the alpha overlay strategy.

These and other alpha strategies aim to better the returns offered by the market risk premium.

An alpha overlay strategy aims to limit overexposure to risks or factors by targeting alpha across different asset classes and factor strategies. This can be used to reduce the correlation within a portfolio and improve diversification, thereby smoothing volatility risk and a fund’s overall risk-adjusted performance.

An alpha overlay strategy can be implemented by using a held investment as a deposit for a futures or forwards contract in another asset class, thereby adding a further and uncorrelated alpha source to a portfolio. By virtue of diversification, this can reduce volatility while bolstering the pool of alpha sources. And since alpha overlay strategies are effected mainly through futures, they require minimal cash outlays.

Beyond alpha overlay strategies, many investors view usual alpha strategies as an important means to control volatility and risk.

As is evidenced by major market bubbles including the global financial crisis of 2007-2008 and the technology bubble of the late 1990s, traditional market indices which weight their constituents by size are inherently risky. Major market indices like the S&P 500 provide investors with a proxy for market, or beta, exposure.

Consider the technology bubble which came to the fore at the turn of the millennium. Prior to the bubble bursting in 2000, major indices had become heavily overweight tech stocks – placing these passive, non-alpha investments in precarious positions with greater investment risk than may have been estimated at the time.

An alpha strategy which targeted value, low size or quality stocks, for example, would likely have been less biased towards tech stocks that had been overvalued by the market.

Meanwhile, other strategies seeking steady returns, including low volatility indices, can unintendedly sacrifice underlying stock quality by including low-volatility assets with weak fundamentals. Including alpha in a low volatility portfolio can improve diversification and assist in risk management.

A low volatility approach to investing is one of many factor strategies, based on analysing the risk and return characteristics of an investment. While some of these aim primarily to control risk, a number of factor styles target alpha returns, or returns which deliver superior risk-adjusted performance metrics.

Common alpha factors include value (where a portfolio favours undervalued stocks and possibly also sells overvalued ones), and momentum. These factors, among a growing number of other identified factors, are harnessed to exploit asset features which carry higher risk premiums than equity markets.

Furthermore, combining value and momentum strategies can generate market-beating risk-adjusted returns while also controlling volatility risks, since these strategies tend to perform at different phases of market cycles – thereby smoothing investment returns.

These and other factors can be harnessed through alternatively-constructed smart beta indices. Many investors view smart beta funds as attractive alternatives to mutual funds, partly because they tend to incur lower fees. This reflects a partial shift from active fund management to passive fund management, though smart beta is effectively an active slant on passive indices.

A number of index providers now offer multifactor indices. These indices include at least two factors believed to yield excess returns, while factor diversification aims to keep risk in check.

Risk premia investing, meanwhile, implements factor strategies through long-short positions, thereby targeting absolute returns irrespective of the performance of markets.

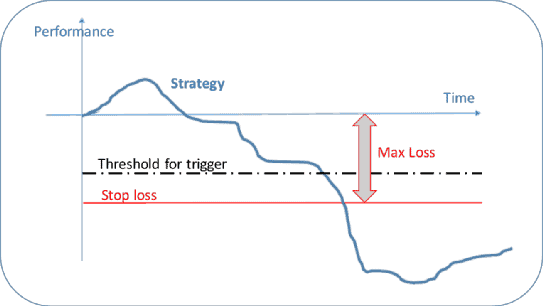

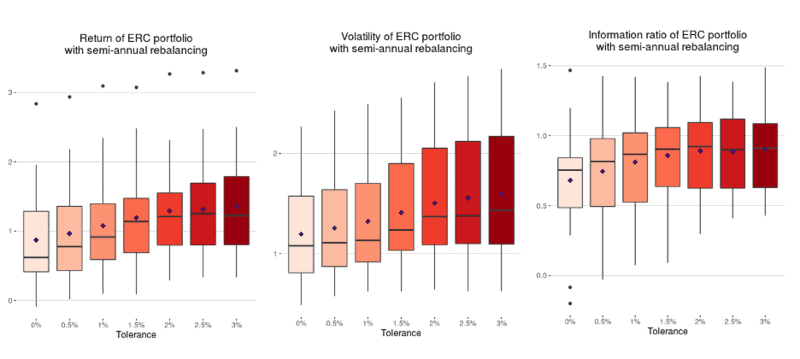

An example of an alpha model specifically targeting volatility

It is widely recognized that predicting returns is a far more difficult task than forecasting volatility, and since the two are not always highly correlated, it is not always easy to forecast returns based on expected volatility.

But a 2010 report called Alpha Generation and Risk Smoothing Using Managed Volatility said that employing a strategy in which returns are a function of volatility can yield market-beating returns while also smoothing volatility risk. The paper, by Tony Cooper, argued that adding leverage to an alpha strategy could help predict returns.

Cooper suggested three leveraged alpha strategies, one of which was called the constant volatility strategy, which aimed to maintain volatility at a specified target by adjusting leverage in response to expected daily volatility. This reduced volatility without placing a drag on returns.

Meanwhile, smart beta indices with a bias towards the low-volatility factor are also often able to generate alpha returns. Index provider BlackRock said recently that the explosive growth expected in the smart beta market will be driven by minimum volatility indices. Smart beta funds are types of proprietary indices. factor analyses to identify characteristics behind better risk-adjusted returns.