Perhaps a reason for the wide array of names for ‘smart beta’ investing is the difficulty of labeling this relatively new strategy. Smart beta strategies differ from risk premia strategies in that smart beta must adhere to long-only positions in assets.Also known as custom indices, self-indexing, factor indices and alternative beta strategies, the world of smart beta investing is still finding its place in financial markets.

Some investors believe the use of beta in the name of the strategy is misleading since these indices often aim to produce superior returns (in other words, alpha rather than beta).

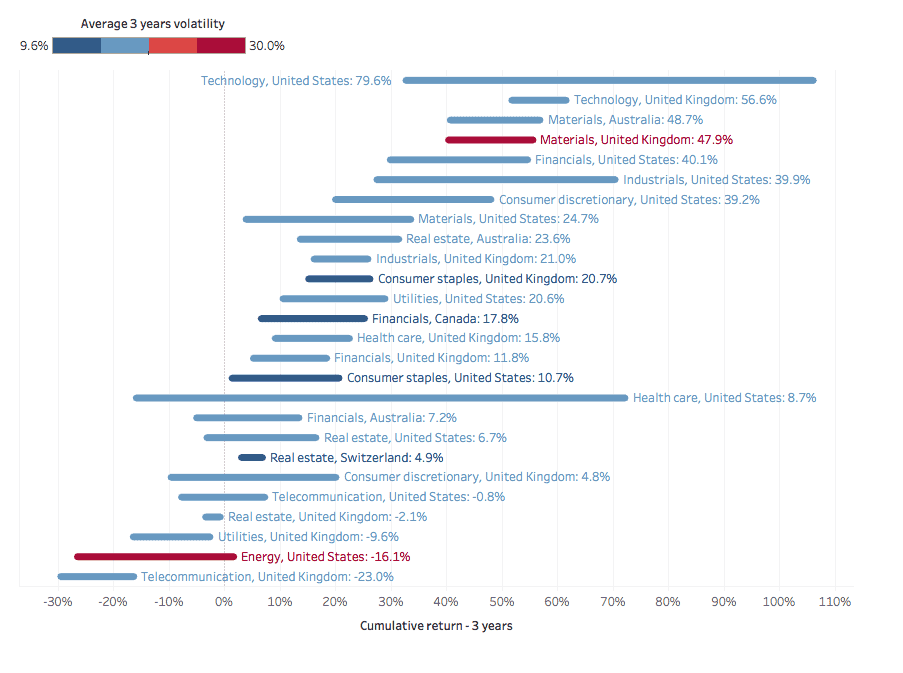

Beta quantifies a stock or fund’s volatility (or risk) relative to the market, where a beta value of 1 implies that the investment will move in toe with the market. A beta of less than 1 suggests less volatility relative to the market while a beta of more than 1 points to more volatility.

Alpha, meanwhile, refers to the extra return yielded by an investment that is the result of identifying and targeting underlying risk factors. Alpha is often seen as the value added by a portfolio manager through good stock selection, or in the case of smart beta products, a superior strategy.

Smart beta indices are alternatively weighted or constructed indices which offer a tilt towards one or more underlying risks. For example, an alternatively-weighted index might assign unconventional weightings to the S&P 500 Index, which weights constituents by size and offers pure beta exposure. The smart beta fund’s performance is compared to the index and is measured on a risk-adjusted basis. A custom index fund might offer a tilt towards value stocks (or those which are undervalued by the market), for example.

By virtue of the fact that smart beta index providers target specific underlying factors in order to generate better returns, these strategies are not entirely passive and the name might not accurately reflect their goals. They are based on quantitative data analyses which aim to identify underlying factors or market abnormalities.

Simply by deviating from pure market (or beta) exposure, smart beta automatically becomes a semi-active approach to investing. The ‘smart’ part of the name is slightly less ambiguous, since it refers to efforts to avoid the market inefficiencies of traditional size-based indices, which can become heavily weighted towards expensive stocks and sectors.

Perhaps smart beta indices are better described as passive investments with an active (alpha) tilt, or as low-cost alpha funds.

Part of the attraction is that by straddling both the passive and active investment world, custom indices can incur the relatively cheap fees associated with passive indices while also offering better returns.

Some smart beta strategies, however, assign a higher priority to risk control than to excess returns. Low-volatility funds, for example, provide a bias towards funds which tend to deliver steady and consistent returns and are less volatile (or risky) than the market. In short, they are valued because they aid in risk management.

Assuming that less risk equals dimmer return prospects (under modern portfolio theory), low-volatility indices are usually not thought of as alpha funds. But many investors believe low-volatility investing can in fact offer superior long-term returns, partly based on criticism of modern portfolio theory. Some market commentators and investors argue that volatility should not be used as a proxy for risk.

Factor investing and alpha returns

Smart beta funds target factors including low volatility, value (by favouring undervalued stocks over expensive ones), and size (by favouring smaller stocks, which tend to outperform over the long term), among others.

These alternative beta sources, as they are sometimes known, can be harnessed by hedge fund replicators.

Hedge funds are notoriously opaque investments and the sources of their returns are often difficult to pinpoint.

Just as smart beta indices are proving an attractive alternative to mutual funds, risk premia strategies offer an alternative source of absolute returns over hedge funds.

Using long-short investment techniques, which can involve buying a smart beta investment and short selling its benchmark, risk premia strategies are gaining in popularity and are increasingly used to substitute for, or complement, hedge funds.

This is partly because of the global push for transparency and portfolio cost management, as well as the trend towards factor-based investing.

Some financial theory models have been expanded to explain why underlying factors such as size and volatility can produce excess returns over the long term.

Some factor-driven models are also proving suitable for faith-based invessting. For example, long-only smart beta investments often meet the strict requirements of Shariah-compliant funds, which could provide a growth opportunity for index providers.