Quantilia chats to Serge Janowski, Global Head of Institutional Clients and Family Offices at Banque Cramer, about factor investing within the institutional market.

Quantilia: Why have quant- or factor-based strategies, such as smart beta and risk premia, become so popular among institutional investors?

SJ: Factor-based indices are receiving a lot of attention partly because they are semi passive, which means costs tend to be lower compared to actively-managed funds. Driven by the low return environment we find ourselves in, there is a push towards reduced fees.

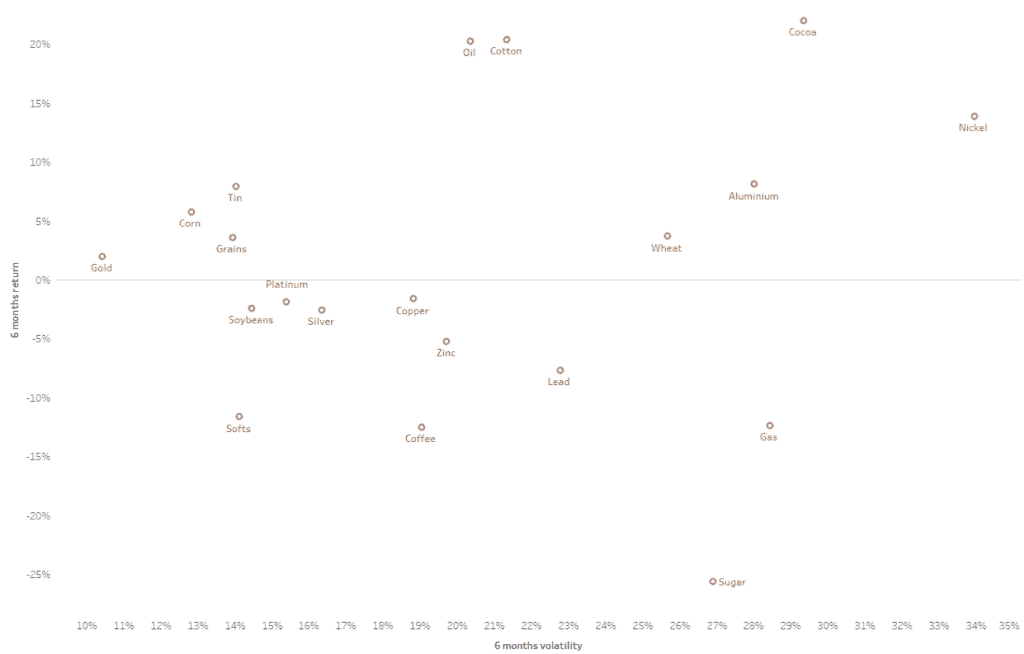

Instead of targeting asset classes, smart beta and risk premia indices target factors which deliver better risk-adjusted returns. Given how volatile markets are, and given the low rate environment, the factors which are particularly popular at the moment are low volatility and high yield.

Compared to retail investors, institutional investors have access to far more smart beta and risk premia products, many of which are tradeable only in OTC markets.

Another driving force behind factor-based indices is that they are rules-based and transparent. Institutional investors are increasingly looking for transparency, and for that reason strategies that adhere to clearly-defined rules are favourable.

For institutional portfolios, factor-based strategies can complement existing allocations and offer an important source of diversification. When it makes sense to do so, especially from a cost point of view, factor-based indices can replace underperforming active allocations.

To get the most out of factor indices, portfolio managers need to select appropriate strategies, time them well, and rebalance portfolios efficiently. The approach to buy and hold funds is not efficient considering that markets are likely to remain unpredictable for some time, which means timing factors is important.

What can a Swiss private bank like Cramer offer in this space?

Europe is a frontrunner in the market for quant strategies, driving much of the innovation behind, and demand for, factor strategies. Switzerland is a key part of that, given its positioning in relation to important markets in Scandinavia, other parts of Europe, and the Middle East.

Private banks like ours are becoming more involved in the asset management side of things. We are building an institutional-focused business, and we believe we understand the needs of institutional investors and can offer them competitive and customised solutions.

There’s been growing interest in solutions which are transparent and cost effective, while still being able to outperform. Cramer is independent, which means we can select the best products available on the market and deliver them to our clients.

We can offer tailored solutions for institutional investors, based on their own needs and on changing market dynamics. Importantly, we can do this in a transparent and cost-effective way.

What impact do black swan events, like Brexit, have on this business?

In a more unpredictable market environment, allocating capital based on the usual asset class split is not efficient enough. There needs to be a heightened focus on specific risks and on underlying sources of performance – something which smart beta and risk premia investing offers.

Some factors showed resilience in the wake of the Brexit vote. Yield stocks, for example, recovered quickly and have performed well since, partly because they offer an alternative to low-yielding bonds.

Will passive investing, including smart beta and risk premia, replace active fund management?

Indeed, we hear that often, but I disagree – there will always be a need for active management, albeit with a different spin. We expect the new game to be a blend of passive and active management, where the focus will be on managing portfolios made up of passive yet sophisticated building blocks – similar to how asset managers built portfolios of securities ten years ago.

Some hedge funds are doing this already, and we expect this to become the new norm.

Which markets offer the best opportunities for this business?

The market for factor-based strategies is rapidly spreading and becoming global. Switzerland, other parts of Europe, and the Middle East are all important for us.

In the Asia-Pacific region, Japan and Australia were early adopters of these strategies. Some specific markets in the region have been very active in this space for a decade already, particularly sovereign wealth funds. Now, other parts of Asia are also starting to look promising, such as Singapore and even China.